PFAN was founded in 2006 to support clean energy and climate entrepreneurs with great ideas who lacked the capacity or funding to realise them and successfully scaled up in the period 2016-2023 during the UNIDO/REEEP hosting period. For 17 years, our international network of local advisors has worked with hundreds of entrepreneurs in low and middle-income countries, helping them become investment-ready and mobilise over USD 3.3 billion in financing, creating transformational impact in the regions where they work and for the populations they serve. In this report, we take the opportunity to look back at PFAN’s work under UNIDO/REEEP hosting, zooming in on some of our notable successes, looking behind the scenes at what makes PFAN tick, meeting the advisors and the projects making it all possible, examining the learnings and assessing our enduring impact and contribution to the climate agenda.

PFAN’s work has been made possible by the generosity of our donors, which over the years have included Australia, Austria, Canada, Japan, Norway, Sweden and the United States. However, as the world changes, so does the outlook of our donors, and their priorities have shifted; likewise, the markets in which we operate have also evolved. Accordingly, in agreement with our donors we are bringing the current chapter of PFAN to a close and reassessing the role and positioning of PFAN for the future.

Despite these programmatic funding challenges and global geo-political market volatility, PFAN has once again produced remarkable achievements and milestones throughout 2023, underscoring our continuing commitment to advancing climate and clean energy projects and businesses.

In 2023, 54 PFAN-supported projects mobilised financing of over USD 332.6 million. Given the reduced availability of programme funding, emphasis was placed on bringing projects from the existing PFAN pipeline to investment readiness and mobilising finance. To facilitate that, we successfully rolled out enhanced transaction management support, provided through specialised Transaction Advisors working closely with both entrepreneurs and existing PFAN Advisors to structure and execute deals, thereby expediting investment, especially in sub-Saharan Africa, where we saw six financial mobilisations.

The results of our work in 2023 at a regional level can be found in the respective regional sections of this report. Of special mention here we would highlight the first financial closures in Sri Lanka, Fiji and Pakistan, the strong results in the Eastern Europe and Central Asia (EECA) region, the successful cooperation with the Cold Chain Innovation Hub in the Philippines, the cooperation with Convergence, UNDP and FREF (Fiji Rural Electrification Fund) on the design of an innovative financing mechanism for the electrification of remote maritime islands in Fiji, the initiation of a Private Equity Fund in Pakistan and the emergence of PFAN-LAC as a distinct programme entity, operating in Latin America and the Caribbean. Further details of these and many other initiatives are provided throughout the report.

Looking towards 2024 and beyond, there is no doubt that project preparation, investment facilitation, and private sector engagement remain of utmost importance in achieving global climate goals. The SMEs we have supported since 2006 have tangibly contributed to advancing low-carbon renewable energy markets and mitigating and adapting to the effects of climate change. However, countless entrepreneurs still need the business know-how and investor introductions that PFAN provides as we collectively work towards reaching the targets of the Paris Agreement and the Sustainable Development Goals.

Accordingly, UNIDO and REEEP are actively exploring new opportunities to harness the legacies of PFAN – the global network of advisors, the robust and deep pipeline, methodologies and systems and not least, the market experience and institutional memory – to continue to work with climate projects and investors, where project preparation and investment facilitation support is most needed.

Marko van Waveren Hogervorst, Eva Kelly and Peter Storey

PFAN Programme Management Unit (PMU)

02

PFAN’S IMPACT IN 2016-2023

How it all started

It was in Bonn in 2006, during a UNFCCC workshop, that PFAN was first mapped out. Peter Storey, PFAN’s Global Coordinator, illustrated the need for a service that would bridge the gap between entrepreneurs with great ideas for climate and clean energy projects and investors. This would take shape through a network of consultants providing targeted advice for entrepreneurs to prepare their projects to attract investment and then introduce them to investors.

Two years later, CTI PFAN was established as a full programme of the CTI (Climate Technology Initiative), supported by a secretariat at ICETT (International Center for Environmental Technology Transfer in Japan). The programme grew significantly in 2009, organising its first Investment Forums in Asia and Africa and gaining support to scale up its activities. Demand for PFAN’s services was so high that by 2016, it was clear that scaling up the programme to its full potential would require a different hosting arrangement and a new organisational structure. Following a competitive bidding process, the United Nations Industrial Development Organization (UNIDO) and the Renewable Energy and Energy Efficiency Partnership (REEEP) were selected as PFAN’s new hosts.

Scaling up

At the first PFAN Steering Committee meeting in December 2016, two resolutions were endorsed to guide PFAN’s future growth plan: first, a resolution on PFAN’s scale-up strategy and second, a resolution on gender mainstreaming.

The essence of the resolution on PFAN’s scale-up was the focus on strengthening project origination through wider and deeper networks and increased number of coaching opportunities, increased interfaces and cooperation with strategic partners and access to wholesale capital markets through bundling and securitisation approaches. The overall objective was to increase the investment leveraged by PFAN-supported projects three-fold, thereby creating the relevant climate impacts in terms of reducing GHG emissions and establishing new clean energy capacity.

Due to changing market circumstances, the strategy for accessing wholesale capital markets needed to be refined and adapted; institutional investors were not ready yet to invest in climate SMEs in developing countries, and the conditions to bundle PFAN projects were not in place both on demand and supply side. Instead, the strategy refocused on co-designing innovative financing instruments with key market players, especially through blended finance techniques, to fill critical gaps in the financing spectrum and create linkages to funds and fund managers.

PFAN has delivered on its growth expectations. The ambitious scale-up target on investment leveraged by PFAN-supported projects has been achieved. In fact, while the COVID-19 pandemic impacted project origination, targets on PFAN-supported projects reaching financial closure have been achieved with a lower budget than initially planned. Thus, PFAN became more efficient during the scale-up phase.

Achievements and impacts

Since inception, PFAN has supported more than 1400 projects and businesses, facilitating the mobilisation of over USD 3.3 billion in investment into more than 260 of them. Most of these results were achieved during the scale-up phase, wherein 869 projects and businesses were supported, 168 of which attracted a total USD 2.16 billion. This significant result has been achieved by outstanding entrepreneurs furthering climate and clean energy solutions, many of whose success stories you can explore throughout this report.

This exponential growth happened on the back of the geographical expansion and deeper networks, including more than 100 local and regional PFAN partners, implemented in the period 2016-2023 under the new hosting structure.

0

1

2

3

3

4

5

6

7

8

9

0

1

2

3

in investment leveragedbillion

2006

2010

2014

2018

2024

17 years later, PFAN has supported more than 1400 projects and is proud to report on its impact of over USD 3.3 billion raised for more than 280 projects.

Total number of projects which mobilised finance 2016-2023

Technology area of projects which mobilised finance 2016-2023

Impact 1: Local climate finance advisory market developer and catalyst

The financial mobilisations have been driven by PFAN’s global network of advisors, consisting of technical and financial experts and transaction advisors, the majority of whom (>95%) are based locally in the countries of PFAN operation. We carefully vet each advisor for their expertise and track record and continually enhance their skills to capacitate and nurture the local financing and advisory ecosystems. Since 2017, the network has grown from some 70 advisors to over 250 today, expanding into new regions (including Eastern Europe and Central Asia, the Pacific Islands, Latin America and the Caribbean), consolidating in existing regions (South Asia, Southeast Asia, West Africa, East Africa and Southern Africa), entering into new countries and going deeper into existing markets.

Regular trainings and capacity building over this time have focussed on gender lens investment, financial modelling, blended finance, carbon finance, transaction management, investment structuring and deal closing. PFAN’s financing advisory footprint is unmatched for its depth and breadth. PFAN not only significantly contributed to building local climate finance advisory ecosystems by capacitating the advisors on the benefits of gender-smart businesses, we also helped to build up local ecosystems that promote gender equality.

Moreover, PFAN served as a facilitator between different market players. By facilitating connections between entrepreneurs and advisors, PFAN bridged a crucial gap, enabling developers to access advisory services that might have otherwise been financially out of reach. As a result, projects were able to access high-quality guidance at a reasonable cost, while PFAN Advisors gained valuable opportunities and revenue streams they might have otherwise overlooked.

PFAN has acted as a market catalyst in other ways, such as partnering with PFAN Advisors to support implementing projects and thereby increasing the sustainability of their advisory businesses. For example, the AgriPitch competition is an excellent example of PFAN’s role in creating self-reliant local financial advisory capacity. Subsequently, more and more PFAN Advisors are becoming independent market players. As a result, the local climate finance advisory industry is developing, resulting in more businesses supporting and entrepreneurs raising funds.

PFAN Advisors in 2023

Get to know some of our advisors here on our ‘Meet the Network’ playlist on YouTube.

Impact 2: Creating financial sustainability of climate businesses

Numerous PFAN projects that mobilised finance kept growing after PFAN services ceased to be provided. Typically, PFAN’s support is catalytic for the entrepreneurs to advance from an early business development stage to investment readiness. The capacity building and mentoring on business and financial modelling development, as well as interactions with investors during the PFAN Journey, aims to enable entrepreneurs to successfully face and negotiate with investors on their own. After receiving PFAN support, many of these projects and businesses raised several rounds of additional financing with no further PFAN involvement – Fourth Partner Energy is an excellent illustration of the long-term impact of creating financial sustainability.

Impact 3: Increased investor confidence

Thanks to PFAN, investors learned about investment opportunities they might otherwise not have considered. Additionally, PFAN supported prospective investors in enhancing their comprehension of low-carbon, climate-resilient investments and assessing and mitigating associated risks. This has been achieved through regular interactions with the investors by the PFAN advisors as well as through specific capacity building activities and investor roundtables and investor events referred to in the regional sections of this report.

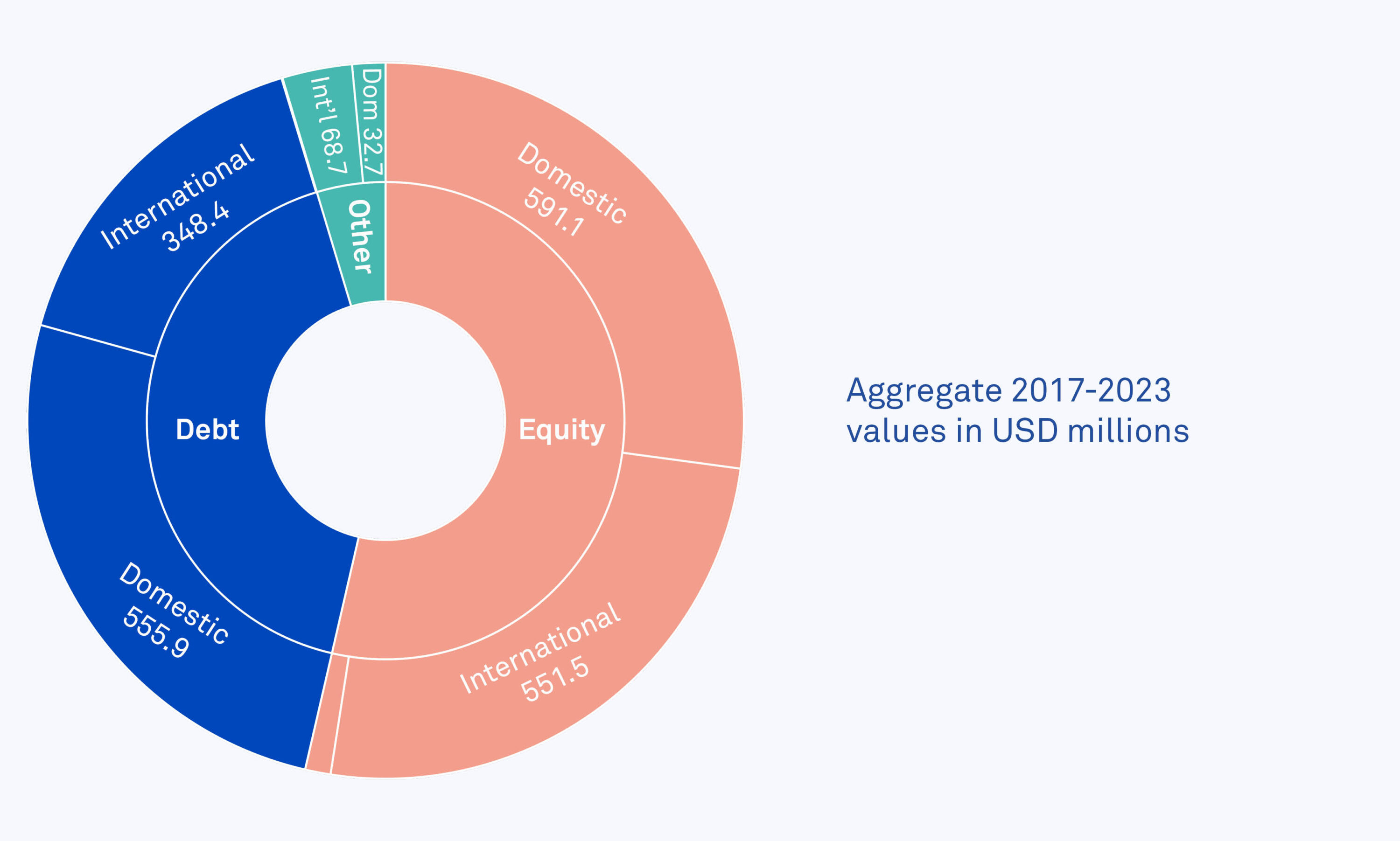

The increasing annual number of financial mobilisations achieved during the period 2016-2023, and the fact that this has predominantly been involving domestic investors, underscores the heightened confidence among investors in general and domestic investors in particular.

Co-designing financial instruments with financial partners in Southern Africa, Fiji and Pakistan will further increase investor confidence in investing in climate businesses directly or indirectly.

Financing raised by investor type (domestic vs. international) and financial instrument

Milestones during the UNIDO/REEEP hosting partnership

2016

PFAN under new hosting structure in Vienna, the first milestone of USD 1 billion in investment leveraged by PFAN-supported projects

PFAN’s holistic approach provides solutions to market challenges in both supply and demand. On the one hand, small and medium-sized businesses in frontier markets lack the capacity and know-how to get their projects off the ground or raise them to the next level. On the other hand, investors are unaware of these promising ventures or are too hesitant to take the plunge.

There are gaps at the ecosystem level and limitations in the capacity and expertise of traditional financing advisory services within those markets, making it tough for financing to flow to where it is most needed. This is where PFAN steps in: deploying targeted and highly specialised technical assistance and creating a more conducive environment where climate and clean energy businesses can thrive. Our work accelerated the deployment of climate solutions, increased investment in climate mitigation and adaptation and successfully unlocked frontier markets. This ultimately leads to a reduction of greenhouse gases, increased climate resilience and enhanced socio-economic development, paving the way for a greener and more resilient future.

Over the years, PFAN has adeptly responded to several developments and trends in the climate finance space by introducing initiatives and programmatic foci, which have not only underscored the programme’s flexibility and adaptability but have also contributed to the programme’s enduring success.

Gender mainstreaming

As noted above, the importance of contributing to gender equality and the empowerment of women was recognised by the PFAN Steering Committee at its first meeting under the new hosting structure in December 2016 with the adoption of a dedicated gender resolution. A timeline of the main PFAN gender activities since 2016 can be found in the gender mainstreaming section of this report and more detailed information on PFAN’s gender indicators and achievements since 2020 can be found in the updated PFAN Gender Strategy for 2023 – 2027launched in 2023.

PFAN has prioritised efforts to include gender equality and the empowerment of women at all levels and in all aspects of operations. Applying a gender lens has been deeply entrenched in all of PFAN’s project development activities: information on a project’s gender focus is requested at the application stage, and it is considered in the evaluation, project development and investment facilitation support services.

The most recent gender mainstreaming activities have included Masterclasses on Gender Lens Investing for our network and the launch of a Gender Action Plan Toolkit. Through these actions, PFAN has not only successfully implemented the gender resolution but also responded to the increasing interest by investors in gender lens investing and contributed to tackling gender inequality, especially in the clean energy space.

PFAN supported women-led or gender-focused projects and businesses which have raised financing between 2016-2023 include:

While investment in clean energy has continued to grow and remains critical, the last few years have seen a relative increase in focus on climate adaptation, with the need for increased resilience dominating the development discourse and focusing the attention of fund managers alike, especially in sub-Saharan Africa. Southeast Asia has also seen increased investment in climate resilience and adaptation, which has been prompted by the severe impacts of climate change, particularly in countries like the Philippines.

While adaptation has gained increased importance, global efforts are still falling behind on financing and implementation. In response, PFAN began actively soliciting applications from projects and businesses that aimed to deliver adaptation-related benefits to their communities in 2019. In 2022, we further intensified efforts to raise awareness of the need for adaptation solutions and organised several events to originate projects with a focus on climate adaptation. For instance, PFAN’s event on the sidelines of COP27 highlighted the actions needed to mobilise the necessary capital to finance climate adaptation projects and businesses and emphasised how the roles of both the public and private sectors are critical in catalysing investment, and showcased three PFAN-supported adaptation projects to present their solutions.

PFAN-supported adaptation projects and businesses which have raised financing between 2016-2023 include:

While the demand for cooling has been constantly growing over the years, it is a significant contributor to global greenhouse gas emissions (on current growth trends, representing 20% of total electricity consumption today1). Therefore, there has been an increasing need for more efficient cooling technologies that are less harmful to the environment. To address this challenge, in 2019 PFAN partnered with the Clean Cooling Collaborative (CCC) to promote energy-efficient cooling in developing countries.

In March 2021, PFAN and CCC held the Cooling Investment Forum, which was attended by more than 300 investors, entrepreneurs and cooling stakeholders. The Forum provided a platform to discuss current cooling investment issues and gave an opportunity for five PFAN-supported cooling projects to pitch in front of potential investors. The joint knowledge accumulated by PFAN and CCC throughout our partnership was condensed in the report “Investing in a Cooler Future for All”.

PFAN-supported cooling projects and businesses which have raised financing between 2016- 2023 include:

The global shift toward electric vehicles (EVs) is necessary for more energy-efficient and climate-resilient mobility. Asian markets are leading the way, especially in 2- and 3-wheeler solutions, and the industry has been enhancing the development of EVs to improve inclusive mobility and support decarbonisation efforts. However, the high capital costs of EVs, mainly due cooling-sector to battery and charging infrastructure, have led to limited opportunities for their growth in low-income countries.

PFAN has supported e-mobility initiatives for over a decade – in 2014, PFAN assisted Ather Energy in preparing its initial business plan, financial projection and investor presentation. Today, Ather has grown to India’s fifth-largest EV two-wheeler manufacturer, raising over USD 300 million in investment. In the ensuing decade, we have helped 45 further clean transport projects find innovative ways of facilitating their growth.

PFAN-supported E-mobility projects and businesses which have raised financing between 2016-2023 include:

In a circular economy, the value of products and materials is maintained for as long as possible. Waste and resource use are minimised, and when a product reaches the end of its life, it is used again to create further value. This can bring significant climate and economic benefits, contributing to innovation, growth and job creation. In 2022, PFAN provided capacity building to our network through a series of webinars where participants learned about and discussed the circular economy, its relevance to PFAN and the type of circular business models PFAN supports.

We also launched a dedicated learning corner, which provides access to recorded webinars and additional learning materials. Moreover, PFAN has put together tips for circular project entrepreneurs on assessing whether their project is circular or how they can better communicate the circularity of their project or business. PFAN-supported projects and businesses in the circular economy space which have raised financing between 2016-2023 include:

PFAN works in low- and middle-income countries all over the world. To ensure locally-based delivery, we have divided our operations into six regions, each with a Regional Coordinator overseeing Country Coordinators and Advisors. Click through each of the sections to find detailed information on the impact we’ve made around the world.

The PFAN Journey is a three-stage process which makes business development more navigable for advisors and entrepreneurs. By responding to individual business needs, the process not only provides PFAN with the flexibility to fast-track projects dependent on their maturity but also enables entrepreneurs to develop their companies based on their specific requirements. Through this process, PFAN has helped over 80 companies (and still counting) successfully attract finance. As an example, we’ve highlighted the Journey of Sun Culture – PFAN’s first company in Sri Lanka to raise finance.

STAGE 1

Action plan

Action plan

Through one-to-one discussions with a locally based PFAN Advisor, opportunities and gaps are identified and entrepreneurs are guided on the necessary steps to success. Together, an Action Plan will be established to make the project or company ready for investor introductions.

Sun Culture’s experience

In the summer of 2022, the entrepreneur Damian Fernando of Sun Culture, a company with four solar PV projects aiming to install PV panels on factory rooftops of apparel companies based in rural areas in Sri Lanka, was introduced to one of PFAN’s Advisors –Piyal Hennayake.

After due diligence on the company, business idea and documents, Piyal helped Damian develop an action plan to improve to sets out the work required under over the following months to ensure the project is ready to meet investors.

STAGE 2

Project development

Project development

During the second stage of the PFAN Journey, our Advisors take a hands-on approach to provide support in different areas explicitly tailored for the entrepreneur and their project. The services range from assistance in securing licenses/permits, developing financial models and refining business plans, creating gender action plans, guidance, and coordination of feasibility studies, among others.

Sun Culture’s experience

Sun Culture for instance had a rather technical business plan, so Piyal helped Damian and his team refine it to attract investors better and draft a pitch deck. Their financial model was also reassessed, with multiple rounds of iteration, Piyal was able to help Damian finalise the model, giving Sun Culture the confidence to start their first project with their own funds and approach investor for their second project.

STAGE 3

Investment facilitation

Investment facilitation

Once the business documents are finalised, PFAN Advisors help entrepreneurs tailor their pitch presentations and teasers, ensuring they are ready for investor introductions. A data room – an online platform with detailed project documents for investors is generated for projects ready for investor introductions. In this final part of the PFAN Journey, our advisors help identify investors, provide introductions and support in negotiations.

Sun Culture’s experience

By the summer of 2023, Sun Culture decided they were ready to start meeting domestic investors. After finalising all the necessary documents, including an investor teaser and the pitch deck, Piyal and Damian set out to meet several private banks to negotiate funding to acquire PV panels, inverters and other necessary equipment, which would enable the generation of 600,000 KWh annually. One domestic bank was particularly interested in what Damien and his team had to offer.

Despite the odds, with Sri Lanka proving to be a challenging economy, having suffered an economic, political and foreign exchange crisis in which gaining funding for renewable energy projects is difficult, this year, Sun Culture raised the funds necessary to kick-start and complete their second project with the help of Piyal and the PFAN team. Having developed a strong relationship with Damian, Piyal aims to continue supporting Sun Culture to ensure they can get their other two projects up and running within the upcoming year.

“Despite the significant advantages of micro-renewable systems for the Sri Lankan environment and economy and their potential for steady income generation, the banks seemed either unaware or hesitant to acknowledge these benefits positively. Our PFAN Advisor’s efforts were instrumental in addressing these concerns, convincing the bank of Sun Culture’s benefits, and helping expedite and secure the loan. He played an active role in the documentation, calculations and reports related to the project, further demonstrating his dedication to its success.’’

Damian Fernando, Director, Sun Culture Private Limited

PFAN’s focus in 2023 was to develop practical action points and tools to apply a gender lens to PFAN’s advisory services. For this purpose, PFAN, in collaboration with Value for Women, has developed a Gender Action Plan toolkit accompanied by self-paced training modules. The main objectives of the tool kit are:

to equip the PFAN network with practical tools to guide entrepreneurs on embedding gender intentionality in their business through the development of a Gender Action Plan and help them to increase the investment readiness of projects.

to support entrepreneurs to establish their baseline gender-responsiveness status and create a roadmap of their intended gender journey. Additional videos that support this process have been developed to support this process.

to guide the Regional Coordinators in the assessment of the Gender Action Plans in alignment with PFAN requirements and the PFAN Gender Marker, a gender self-assessment for the businesses and advisors.

The development of the toolkit is based on capacity building for the network throughout the years, in which PFAN has provided gender awareness trainings as well as Masterclasses on Gender Lens Investing to our network of advisors – ensuring that gender is integrated throughout the coaching process. This has also been reflected in PFAN’s evaluation tools, application and reporting forms.

Gender Action Plans

As Gender Lens Investing is increasingly important, our initiatives on gender mainstreaming should not only contribute to making more businesses gender-responsive but also to help more of them reach financial closure. The development and implementation of Gender Action Plans is increasingly a requirement of investors, as illustrated by an example from sub-Saharan Africa:

Bio-Innovations, a biomass waste-to-energy company in Uganda, which raised debt of USD 40,000 was requested by their investor to develop a gender action plan as a condition precedent to receive the requested financing. The PFAN Advisor not only helped the entrepreneur and his company to understand which steps he’d already taken towards a gender inclusive business, but also helped him to set new goals and actions for implementation. They developed steps to increase diversity in the workforce, raise awareness of gender equality within the company, design marketing and sales strategies to appeal to and increase female customers and a method to collect and analyse sex-disaggregated data.

Watch how Bio-Innovations is working to turn agricultural and forestry waste into clean burning briquettes.

In 2024, there will be an increasing focus on developing Gender Action Plans for the projects PFAN is supporting in the regions where we remain active. In Southeast Asia it is envisaged that five projects will be supported to develop their plans. In Pakistan, PFAN Advisors have received additional trainings on how to develop a Gender Action Plan, and four businesses will receive support in setting up a concrete plan to improve gender responsiveness in the coming year.

Highlights in 2023

The Pakistan Private Sector Energy (PPSE) project has been particularly active, with two events focusing on gender mainstreaming in 2023:

a 1-day intensive training covering the gender lens within banking products that facilitate more equitable investment, particularly in clean energy. PPSE partnered with the National Institute of Banking and Finance (NIBAF) for this capacity-building initiative, which resulted in 59 finance professionals from 44 institutions trained in Gender Lens Investing.

an online demo session on “Developing the Business Case for Gender Lens Investment in Banking Product Design”. The session was led by Fauziah Ali Banuri, Divisional Head of Marketing at Bank of Khyber who took 28 participants from financial institutions and investment hubs through a gender assessment toolkit formulated by the Financial Alliance for Women.

While we have made significant advances and we can see investors increasingly emphasising the importance of gender impact in the projects they finance, PFAN’s continued work on gender mainstreaming is crucial. As the chart below shows, there have been improvements over the years, particularly in the numbers of women-led projects that have raised finance, but there is still much work to be done:

Indicator

2021

2022

2023

Women-led projects supported

24,5%

24,9%

16,1%

Women-led projects which raised finance

4,9%

19,2%

18,4%

We would like to highlight the following seven women-led businesses which have raised finance in 2023 (under the PFAN definition, a business is considered women-led if 50% shares, or more, are held by women or at least 50% of the management team are women):

Company

Country

Sector

Description

Simusolar

Tanzania

Solar

Simusolar is a provider of solar productive use solutions, including solar water pumps, solar fishing lights, solar security lights and solar refrigerators. Solar irrigation will ease women’s work in the agriculture sector and limit the need to carry heavy water at long distances to irrigate the land. Aware of the need for gender equality, the business has achieved a respectable representation of women in the management team and in the overall workforce.

Solar Nation SMC LTD

Uganda

Solar

Solar Nation delivers its clients a fully installed PV system with items that include a charge controller, power inverters and storage batteries supporting energy generation, storage and dispensing to the selected loads. In order to increase their gender responsiveness, the company aims to increase its number of women to at least 50% of the workforce. They have worked with training associations such as SENDEA Uganda to help achieve this goal.

Little Sun Zambia Limited

Zambia

Rural electrification and energy access

Little Sun is a social business providing solar energy and technology services to households, small businesses and small holder farmers. The project benefits women by aiming to have a workforce of 50% women and decreasing their daily risks through the use of solar equipment instead of firewood collection. Furthermore, by acquiring Little Sun’s affordable equipment, women-led businesses have seen a boost with easier access to energy.

Wiibike Vietnam Technology Joint Stock Company

Vietnam

Clean transport

Wiibike develop sand distributes electric bicycles. With gender ownership and executive management of women at 60%, the company aims to help those with busy schedules get around quicker, faster and cleaner with their e-bikes, which are increasingly promoted to women in urban areas.

SRL “SunGa”

Moldova

Solar

SunGa is building a photovoltaic power plant to generate electricity. With the company’s owner being a woman, she aims to provide equal opportunities to women in the workforce, aiming for at least 50% of the jobs created for women.

Vanrik Agro Group

Kazakhstan

Agriculture

Vanrik Agro is involved in the industrial cultivation of blueberries and the creation of a plant cloning centre. The company sees gender equality as one of its key daily activities. It consists of a team that sees no gender differences, which they have reflected upon through training to increase awareness of gender mainstreaming and develop a Gender Impact Assessment.

Husk Power Nepal Pvt. Ltd

Nepal

Biomass

Husk Power makes energy efficient clean cook stoves, particularly for farmers and rural populations. The company has included women at multiple levels of the value chain and sees them to be a critical part of the project. Women are the primary direct beneficiaries of the improved cookstoves, which has led to reduced time spent on collecting firewood, cleaner cooking environments and less exposure to indoor air pollution, irritable eyes and respiratory diseases from burning firewood

PFAN’s gender activities since 2016

2016

Adoption of PFAN Gender Resolution

Establishment of the PFAN Gender Ambassador

2017

Collaboration and knowledge exchange with local partners

Targeted calls for proposal in West Africa and Asia

2018

Development of a Women-led Clean Energy Business Toolkit

Deep dive workshops in Asia

Global Forum in Vienna

2019

Development of a Gender Strategy and action plan

Gender disaggregation of data in application form

2020

Gender disaggregation of the log frame

Gender awareness webinars to the network

2021

Work with VfW on Masterclasses

Gender-targeted campaigns on social media

Participation in events and panel discussions

Data analysis of the PFAN pipeline

2022

Refinements with regards to gender in application form, reporting and evaluation

Established Gender Focal Points

Continued work with VfW

2023

Launch of Gender Action Plan Toolkit

Self-paced training modules

New PFAN Gender Strategy

Over the last two years, PFAN partnered with ADEME (the French Agency for Ecological Transition) on a special collaboration to support entrepreneurs who are developing and implementing innovative solutions to improve off-grid energy access in sub-Saharan Africa. The main priorities were to build the capacity of local players to ensure sustainable benefits for local populations and to enable the creation of income-generating activities for agricultural producers and micro-entrepreneurs.

ADEME launched the call for projects inthe region’s French-speaking countries, and PFAN provided technical assistance and an impact evaluation to 9 selected companies in Benin, Burkina Faso, Cote d’Ivoire, Madagascar, Senegal and Togo. These companies were working with a variety of technological solutions to deliver reliable off-grid energy to their customers – powered by solar or the processing of agricultural waste – as well as experimenting with new payment and governance systems adapted to local needs and providing training activities for their agents.

While ADEME supported the companies initially through grants, PFAN provided business advice and helped them in the evaluation of their impacts. PFAN gave guidance on economic feasibility, project structure and business plan preparation as well as facilitated introductions to investors. We selected Impact Amplifier, a specialised advisory firm from South Africa, to conduct the impact assessment in parallel to the financial advisory services provided by PFAN. They supplied a detailed assessment of the companies’ specific needs as well as capacity building on the use of methodologies for identifying, monitoring and evaluating those impacts.

The selected companies were further supported with professional videos for use in their fundraising efforts. PFAN worked with the local project teams and videographers in the respective countries to create inspiring stories that illustrate the direct impact these businesses have on the local population. We are particularly proud that MOON, a solar company based and operating in Senegal and Togo won the “Solar Video of the Year” at the AFSIA Awards 2023 for the video we produced. The video, which is also available in French, illustrates how MOON’s energy access solutions are providing everything from increased learning opportunities to productive use of energy for agriculture to improved night time security in off-grid communities in Senegal.

Watch the AFSIA winner for ”Solar Video of the Year” on MOON, an energy access company in Senegal and Togo. Credit: Audy Valera.

One of the main learnings during the collaboration was that, with increasing expectations from financiers – such as impact investors – to deliver on impact data as well as having a business plan and financial details ready, PFAN type of support is needed in the market. At the same time, it has become increasingly challenging for small enterprises to raise funds, which is why public contributions and grants to help the projects get off the ground and keep their operations going are ever more relevant. The combination of PFAN’s technical assistance and early-stage grant support, as provided by ADEME, can therefore be seen as a potent instrument for project preparation and pipeline development. PFAN would like to extend its thanks to ADEME for the opportunity to cooperate on this initiative.

08

Pakistan Private Sector Energy Project

PFAN launched the Pakistan Private Sector Energy Project (PPSE) in 2021 with the goal of expanding the portfolio of commercially-viable clean energy projects in Pakistan and providing support to enable them to build their capacity and access financing.

Supported by USAID, the project targets small and medium-sized enterprises (SMEs) in Pakistan, including those located in industrial zones, while also addressing the needs of isolated communities through off-grid solutions.

Pakistan Private Sector Energy Project Annual Report 2023

Visit the PPSE section of this Annual Report for detailed information on its activities in 2023.

As the UNIDO/REEEP hosting structure comes to an end in 2024, PFAN will primarily focus our activities on two programmes funded by the United States Agency for International Development (USAID) – PFAN-LAC in the Caribbean and the Pakistan Private Sector Energy Project (PPSE).

Starting from February 2024, REEEP and its partner Innovación Social y Ambiental (ISA) will operate PFAN-LAC as the Project Preparation Facility (PPF) for the Caribbean Climate Investment Program (CCIP) under the United States Agency for International Development (USAID)’s Climate Finance for Development Accelerator (CFDA). Under the scope of the PPF, the regional activities will involve developing a pipeline of renewable energy, energy efficiency and climate adaptation projects at different stages of the pre-investment cycle, and to continue to provide advisory and investment facilitation services to the projects in the pipeline through the existing highly skilled network members in the region. Over the coming three years, PFAN-LAC aims to mobilise finance for climate change mitigation and adaptation by providing advisory services to at least 40 promising projects in the region.

PPSE will focus its activities in the coming year on investment facilitation for high-potential projects as well as setting up a Private Equity Fund. Overall, 20 projects are expected to be supported via transaction advisory services. Moreover, capacity building and market awareness boosting activities will involve 5-8 events organised in collaboration with the National Institute of Banking & Finance (NIBAF) on environmental, social and governance (ESG) issues and Gender Lens Investment trainings for financial institutions. There will also be four investor roadshows (three of which will be organised outside Pakistan) and one advisor meeting event. Finally, research activities will be conducted to investigate Pakistan’s current status and future potential in the EV market, as well as capacity building and training events with public sector institutions.

PFAN’s success over the years has been built on the excellence and depth of our global network of advisors, the proximity to markets that this brings, the tried and tested but constantly evolving methodologies and supporting systems, and the strong and diverse project pipeline. These key assets will remain at the core of PFAN as we explore new avenues with new and existing donors and funding partners in the future, particularly focussing on responding to differing market scenarios and requirements, building project portfolios closely attuned to investor appetites and providing value-added analysis and knowledge products in the most challenging markets. Looking ahead, our ability to provide strategic project development and investment support in the face of shifting investment appetites, address financial structuring and risk mitigation challenges and navigate diverse policy landscapes will ensure that PFAN remains a relevant player in project preparation and investment support for climate projects (with an increasing focus on adaptation), helping thereby to increase resilience and sustainability and drive transformational impact.

10

MEET THE DONORS

During the 2016-2023 scale-up phase, PFAN has been generously supported by the Norwegian Ministry of Foreign Affairs (NORAD), the Swedish International Development Cooperation Agency (SIDA), the United States Agency for International Development (USAID), the Department of Foreign Affairs and Trade of Australia (DFAT), the Clean Cooling Collaborative (formerly K-CEP), Convergence Finance, the French Agency for Ecological Transition (ADEME) and the Ministry of Economy, Trade and Industry of Japan (METI) and BMDW – Austrian Federal Ministry for Digital and Economic Affairs.

Each of these donors brought unique perspectives, resources, expertise and direction to PFAN, thereby contributing to our success in mobilising private financing for clean energy and climate adaptation projects and creating sustainable impacts in the countries where PFAN operates. PFAN would hereby like to extend its thanks to all the donors for their support and high levels of engagement during the 2016-2023 scale-up phase.

Donors’ perspectives on PFAN

As members of the PFAN Steering Committee, our donors offer a distinctive viewpoint on the programme’s impact and effectiveness in implementing entrepreneurial support and accelerating innovative climate solutions towards financial closure. Their perspectives encompass an understanding of the challenges encountered and the lessons learnt throughout the implementation phase. We invited several of our main donors to provide reflections and insights into their experience with PFAN.

Interview

NORAD: Norway has provided financial support to PFAN since 2016, coinciding with the beginning of UNIDO’s hosting period of the programme. My experience with PFAN’s implementation over the years has been highly positive. One standout aspect has been the exemplary management of the programme, characterised by efficiency, cost-effectiveness, and the attainment of significant results. What was noteworthy is PFAN’s emphasis on working with local advisors and obtaining local funding from local investors and financiers. Moreover, PFAN’s robust reporting structure has made it easy to identify changes and monitor progress effectively.

SIDA: SIDA has supported PFAN since 2016, when the Swedish Power Africa team made a pivotal decision to extend support to PFAN, marking the inaugural contribution in what has now become a diverse array of investments. PFAN was a first-of-its-kind initiative in providing business advisory services to SMEs in development and climate-focused sectors. PFAN thereby demonstrated a new model of how this marked need could be addressed and can also be considered to have inspired subsequent initiatives addressing this market gap.

NORAD: One prominent change is the diversification of markets, ranging from large-volume, mature markets to still-nascent ones, necessitating tailored business development support aligned with national and regional development contexts. PFAN has adeptly addressed this by relying on a locally based advisory pool with excellent contextual understanding. Additionally, banks and other financial institutions are imposing stricter requirements for considering investments in developing countries. PFAN has responded by collaborating closely with investors to understand their needs and has taken the proactive step to adapt these insights into its project advisory services. This approach ensures that PFAN’s services remain aligned with the evolving expectations and criteria set by financial stakeholders, enabling smoother facilitation of investments in developing country markets. Finally, PFAN has enhanced its role in climate adaptation efforts by integrating climate adaptation metrics. In doing so, PFAN ensures its interventions contribute significantly to building resilience in vulnerable communities.

SIDA:The market has undergone significant changes and presented notable challenges, particularly in supporting SMEs, which play a crucial role in development within SIDA’s target markets. SMEs encounter obstacles such as insufficient financing, perceived risk, limited access to fundraising platforms, networks, and business development skills, and challenging business climates. The project and business development phases are lengthy, risky, and expensive, exacerbating these challenges. In response, PFAN has adapted by offering a wide range of services tailored to different businesses and growth stages, addressing the complexities and dynamism of the environments in which they operate. PFAN’s success in supporting SMEs is attributed to its emphasis on local and contextual relevance, which was achieved through the establishment of local networks and consultants. This approach aligns closely with SIDA’s priorities for local integration and ownership, enhancing the effectiveness and impact of PFAN’s initiatives in fostering sustainable development.

NORAD: Throughout my involvement with PFAN, sitting on its Steering Committee has been great fun and a rewarding experience characterised by interactive and engaging management. The donor group’s active engagement in the programme’s development has also been noteworthy.

One significant learning has been the importance of implementing a reward system for business advisory services. Such a system is critical for attracting diversified expertise and enhancing the overall effectiveness of the programme. However, there’s a need to strike a balance between individually based rewards and incentives for collaborative advisory efforts, particularly when addressing complex business needs.

Another key reflection stems from the realisation that many small businesses face challenges in meeting donors’ rigorous accountability criteria. These criteria, which include applying for funds from international financiers and reporting on development impacts over several years, often pose significant transaction costs. Finding ways to streamline these processes is essential to support small businesses effectively.

SIDA: Our partnership with the PFAN team, UNIDO and REEEP has been invaluable to SIDA, fostering long-term commitments and adding significant value to our portfolio companies. The exchange of knowledge has been particularly enriching, benefiting both our companies and SIDA alike. Throughout the development of our portfolio of contributions, the PFAN team has served as a trusted discussion partner, offering insights into the challenges faced by project developers. These dialogues have not only inspired and informed us but have also guided the development and launch of complementary financing instruments, such as challenge funds and procurement approaches utilising results-based financing. Furthermore, they have facilitated our engagement with debt providers, to whom SIDA has extended its guarantee instrument. Being part of PFAN since its inception has been a source of pleasure and pride for SIDA. We have witnessed its growth into a recognised market player in the field, further affirming the significance of our collaboration.

NORAD: PFAN’s contributions have been instrumental in advancing NORAD’s objectives and enhancing its development cooperation efforts in the realm of climate finance and sustainable development. By working closely with small and medium enterprises, PFAN has played a crucial role in mobilising commercial climate finance, filling a vital niche in this area and contributing to achieving NORAD’s CO2 emission reduction and climate investment targets. Moreover, PFAN has influenced NORAD’s development cooperation work by strengthening the agency’s understanding of the importance of project preparation. This has led NORAD to develop its private sector approach, drawing on positive learnings from PFAN’s experiences. Initiatives such as supporting incubators for nascent companies and gaining a better understanding of the project development lifecycle have been initiated, informed by discussions with PFAN management and other donors.

SIDA: PFAN has significantly contributed to advancing SIDA’s strategic objectives, particularly in increasing production and access to renewable energy, improving conditions for decent and productive jobs, and enhancing resilience to some extent. PFAN’s catalytic approach is exemplary in mobilising private sector resources for development in other sectors, serving as a valuable complement to our agency’s contributions and instruments. Positioned between challenge funds and guarantees, PFAN effectively bridges the gap, providing essential support to businesses and initiatives that align with our agency’s overarching goals. As such, PFAN has both directly and indirectly influenced our development cooperation work by enhancing our understanding of catalytic approaches and demonstrating effective strategies for leveraging private sector resources to drive sustainable development.

USAID: In my opinion, the PFAN country programme in Pakistan has resulted in notable success. This outcome is largely attributed to the high demand within the Pakistani market for a structured support system tailored to the needs of the cleantech sector, SMEs, and particularly the nascent electric vehicle (EV) and electric mobility sector. The introduction of the PFAN model addressed this demand effectively, providing support and guidance to stakeholders in these emerging sectors. Despite the challenging environment (fluctuation of the national currency, government transition, ongoing development of policy frameworks), we managed to establish an Accelerator for SMEs, which builds the entrepreneurs’ capacities and prepares them to engage effectively with investors and a Project Preparation Facility, which provides tailored transaction advisory services. These two activities created traction in the Pakistani market and supported the development of the ecosystem. Additionally, we have gathered numerous insights through the implementation of country-specific capacity building activities, a community of practice and market studies. These insights have not only enriched our understanding but have also been instrumental in informing and enhancing the global program across various levels. One notable instance is the integration of gender action planning and gender considerations into transaction advisory services, a practice that was previously lacking specificity. This strategic shift underscores our commitment to promoting gender equality and women’s economic empowerment within our programmes.

The PFAN model’s success in Pakistan can be replicated in other countries, provided adaptations are made to suit local market needs. The model’s efficacy lies in addressing both upstream and downstream demands in the cleantech and SME sectors, alongside capacity building and collaboration with relevant stakeholders. With dedicated funding, similar programmes can be implemented elsewhere, following thorough market assessments to tailor approaches accordingly. While challenges may vary, the core principles of the PFAN model offer a solid framework for driving sustainable development and investment globally.

From 2016-2023, PFAN has been generously supported by our donors: